In a bid to boost economic growth and development, the Federal Government has reiterated its commitment to expanding access to finance for Micro, Small, and Medium Enterprises (MSMEs), manufacturers, and individuals, which are key drivers of economic resilience and job creation in the country.

The Honourable Minister of State for Finance, Dr. Doris Uzoka-Anite gave the assurance today in her office in Abuja, when the Board Members of the National Credit Guarantee Company Limited (NCGC), led by its Managing Director/Chief Executive Officer, Mr. Bonaventure E. Okhaimo paid her a courtesy visit.

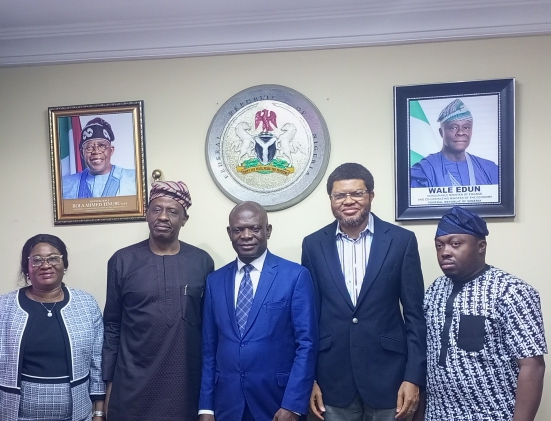

1. Permanent Secretary, Federal Ministry of Finance, Mrs Lydia Shehu Jafiya,

2. Mr Bonaventure E. Okhaimo, Managing Director/Chief Executive Officer of the National Credit Guarantee Company Limited (NCGC),

3. Dr. Doris Uzoka-Anite, Honourable Minister of State, Finance,

4.Tinuola Aigwedo, Executive Director, Strategy and Operations NCGC, and

5. Prof. Ezekiel Oseni, Executive Director, Risk Management, NCGC, in a group photograph shortly after the courtesy call on the Honourable Minister of State for Finance Dr Doris Uzoka-Anite today in her office in Abuja

She praised the NCGC leadership for the rapid and professional manner in which the Company was established, aligning with President Bola Ahmed Tinubu’s Renewed Hope Agenda to strengthen Nigeria’s industrial capacity and foster inclusive growth.

The Minister stated that the success of any institution rests on the calibre of its people. I have full confidence in the leadership and management of the National Credit Guarantee Company Limited to deliver on this vital mandate, she said.

Dr Uzoka-Anite emphasized that the Ministry of Finance will continue to provide institutional support and guidance to ensure NCGC delivers on its role of sharing up to 60% of credit risk with financial institutions, which will help unlock the much-needed financing for MSMEs and manufacturers, facilitate diversification, and cushion the economy against external shocks.

Speaking earlier, the Managing Director/Chief Executive Officer of NCGC, Mr. Bonaventure Okhaimo expressed his appreciation to the Minister for her encouragement and pledged that NCGC would remain steadfast in its mission to catalyse credit access across the country, while also assuring of the organisation’s commitment to accelerating credit access across the nation. We are structured to provide assurance to lenders, thereby stimulating credit flow to productive sectors of the economy, Okhaimo said

In her remarks, the Permanent Secretary, Federal Ministry of Finance, Mrs. Lydia Shehu Jafiya commended the progress in launching NCGC and reaffirmed the Ministry’s readiness to support this institution.

We commend the progress in launching NCGC and reaffirm the Ministry’s readiness to support this institution fully. With the right structures and leadership now in place, we are confident the company will play a transformative role in de-risking lending and empowering SMEs and manufacturers.

The National Credit Guarantee Company Limited, which now reports to the Federal Ministry of Finance, is one of the newest agencies created by the Federal Government. Its establishment marks a significant step toward bridging structural financing gaps, promoting industrial advancement, and broadening financial inclusion.

Signed

Mohammed Manga FCAI

Director, Information and Public Relations